/>

/>

Australian Rare Earth Elements- Issues

Rare Earth Elements Gossip with Sparty

Page Topics

- China's attitude

- Minerals of critical concern

- Alternatives to China's dominance

- World Rare Earth Elements deposits by Country

- Mt Weld (LYC): The world's richest rare earth deposit

- Dubbo DZP (ALK) The world's richest Heavy REE deposit

- Interactive Map of Australia's JORC REE deposits

Rare Earth Oxides are widely seen as being the rate limiting step for the 21st Century's Electron-Economy.

"There is oil in the Middle East. There is Rare Earth in China". Deng Xiaoping (1992)

That same year, the State Council approved the establishment of the Baotou Rare Earth Hi-tech Industrial Development Zone. During his 1999 visit to Baotou, President Jiang Zemin wrote, "Improve the development and applications of rare earth, and change the resource advantage into economic superiority." Then President Jiang repeated the strategic importance of developing China's rare earth industry, which has caught worldwide attention. "The reason why rare earth, a small industry with annual consumption of only 75,000 tons REO and a market value below US$100 million, has been given attention by Chinese leaders at all levels is due to its uses in modern hi-tech industries because of its special chemical and physical properties. As a matter of fact, rare earth has been listed in the category of strategic elements in many countries, such as the USA and Japan. Some experts predict technological innovation will be impossible without the global development and application of rare earth." Read more

As can be seen by the chart above China acted on Deng Xiaoping and President Jiang's directives and now in 2010 is the world's dominant (only) supplier of Rare Earth Oxides. Recently there has been world-wide discussion and recognition of the downside that exists when one country controls the destiny of the world's electron economy.

China currently (2010) accounts for about 96 percent of global rare earth elements production. Of a total production of 120,000 metric tons, about 55,000 metric tons was produced as a byproduct of the Bayan Obo iron mine. This fact means that at least 44 percent of world rare earth elements production is a by-product. Of the remaining Chinese production, about 25,000 metric tons is produced in southern China as a primary product from ion-adsorption clay deposits. The status of remaining Chinese production is unclear. The balance of global REE production is as a by-product. Conceivably, as much as 90 percent of global rare earth elements production is as a by-product or co-product. US Geological Survey 2010

These articles outlines aspects of REEs as currently viewed by China.

- China's new rule to make sustainable use of rare earth, iron, vanadium and titanium. (15/02/2011)

- Experts urge sustainablity in rare earth industry

- Rare earth to be linked

- China, Japan debate restrictions on rare earth exports

- 5 southern China provinces to jointly oversee rare earth mining

- 'Bigger say' set on rare earths market

- Foreigners invest in rare earth deep processing in China

- Chinalco steps up drive for rare earths

- When China's rare earth elements can become rare?

- China to cap nonferrous metals production

- China's biggest metals trader to invest 1 bln yuan in rare earth processing in Jiangxi

China Policy on Rare Earth Update: China further tightens Rare Earth Production and Exports

"The Ministry of Commerce of the People’s Republic of China released a dramatic cut in the second half of 2010 Rare Earths export quota. In total the export quota for 2010 was 40% less than the total export quota for 2009."

"This 40% reduction is a significant decrease in product availability for export which is likely to significantly reduce any remaining stocks in inventory through the supply chain outside China and put pressure on increasing prices. Below is a table setting out the Chinese Rare Earths export quota for foreign invested firms and local firms for the past two years.".....From Lynas Corp's June 2010 Quarterly Report

Ed. Note the massive reductions in REE export quotas from the first half of 2010 to the second half of 2010.

Mineral Raw Materials of Critical Concern

In two recent studies the USGS and European Union studies of mineral supply risk, REE rank highest as mineral raw materials of critical concern, given uncertain future supplies and their importance to advanced industrial economies.

Image below added 11/11/2015

Update: Mineral Raw Materials of Critical Concern: DOD 2016

Three Department of Defense (DOD) offices have identified certain rare earth materials (rare earths) as critical for some defense applications, such as lasers, but DOD has not taken a comprehensive, department-wide approach to identifying which rare earths, if any, are critical to national security. Specifically, DOD offices have not yet agreed on what constitutes “critical” rare earths. Using different statutorily-based definitions, these offices have identified 15 of the 17 rare earths as critical over the last 5 years (see table below)

.

.

Criticality matrix for selected imported metals (USA National Research Council, 2008)

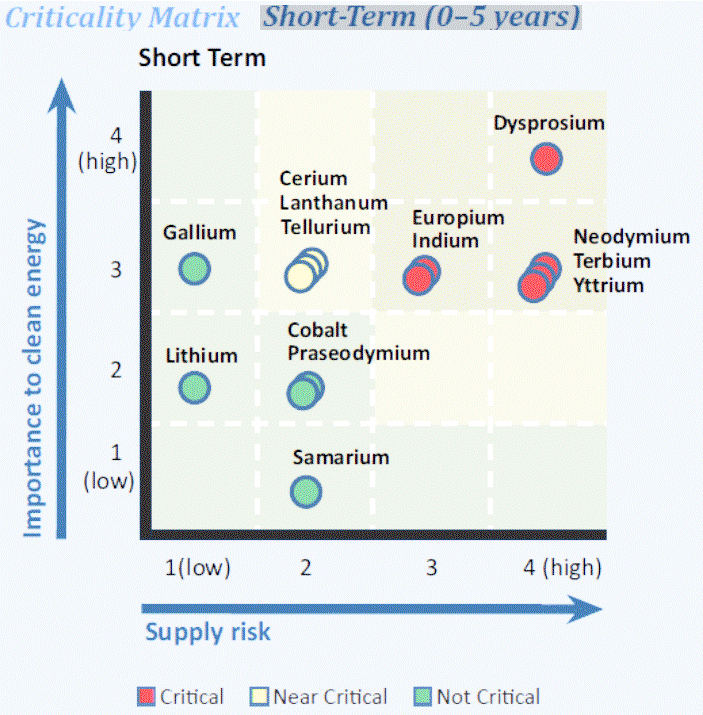

Short term, 0 - 5 years, Criticality Matrix for Green Technology Substrates

(US Department of Energy 2010)

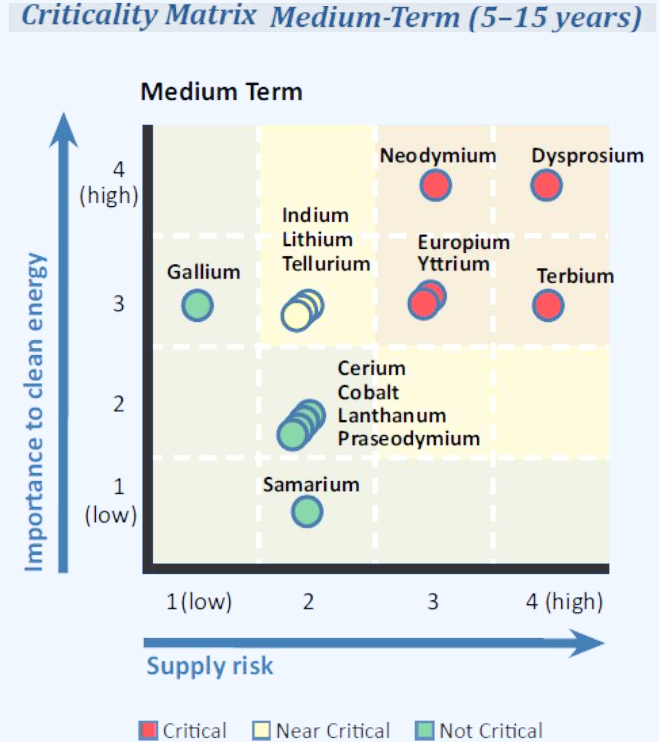

Long term, 5 -15 years, Criticality Matrix for Green Technology Substrates

(US Department of Energy 2010)

From http://www.energy.gov/news/documents...ls_Summary.pdf

http://www.energy.gov/criticalmaterialsstrategy Full paper

Ed. Note: Investors are advised to look at Alkane Resources DZP distribution (below)

Alternatives to China's Dominance

The solution to this current problem of Chinese dominance, outlined above, probably lies within several Australian companies with substantial (JORC) Rare Earth Deposits. The problem is that Australia's Rare Earth Companies have small market caps, with all but one (Lynas Corp) having market caps of less than $245m and consequently are very vulnerable. In total the market caps of all of Australia's companies with JORC REE deposits is less than $1.5b (8/08/2016) and our Australian Federal Government and State Governments have not taken a helpful let alone a pro-active stance by providing project finance or easing the barriers due to excessive permitting restrictions.

Lynas Corp the owner of the world's richest Rare Earth Deposit at Mt Weld, Western Australia now has a market cap of just over $240m (8/08/2016) and is currently mining Rare Earth Elements and producing Rare Earth Oxides concentrates. Lynas has establised a large processing facility, in Malaysia, to produce the highly valuable Rare Earth Metals.

- Lynas Corp JP Morgan New York Presentation 28/09/2010

- Current Status of the Rare Earths Project as at 16 Mar 2011

One Australian company Arufura Resources (ASX Code: ARU) has seen China based interests take a major stake, however the tide to China's world wide dominance of the REEs supply chain might be turning with Australia's Foreign Investment Review Board (FIRB) (October 09) rejecting a 51% bid by China Non-Ferrous Metal Mining (CNMC) that would have seen the world's richest deposit Mt Weld* held by Lynas Corp's ASX: LYC with CNMC as its majority shareholder. The heat is now on for another very large Australian held deposit by Greenland Energy and Minerals ASX: GGG in Greenland where much political manouvering is currently occurring. Recent changes to Greenland's policy on Uranium mining may have seen a new pathway to the development of a world class mining project.

The processing of China's abundant REEs to the usable RE Metals in the past allowed China to dominate the international market as when they felt threatend they could flood the market with Rare Earth Metals and drive other countries out of the market. This situation has changed on two major fronts:

China now probably needs nearly all of the RE Metals that it can produce to satisfy its own internal demand and as mentioned Australia is about to become a Rare Earth Metals supplier in its own right. Consequently Australia may well become the world's swing producer of Rare Earth Elements in the near future and could even break China's dominant Rare Earth Metals supplier position, if our Australian investment community begins to provide support.

Australia as the world's swing producer was an unlikely scenario several years ago but recently three major factors have emerged:

- Australian companies now hold almost as much rare earth elements resources as does China. In terms of proven REE resources per capita Australia has the world's second richest population.

- Australia could become a major rare earth oxide concentrate and processed metals producer.

- China is no longer in the position of be readily able to kill off their competitors by dropping Rare Earth metals supplies to below cost of production as they are barely keeping up with their domestic demand and have imposed export bans, tariff's and quotas as described in the articles above to protect their manufacturing industries futures.

And now that countries like Korea, Japan and the USA have suddenly woken up to the fact that their ticket to the 21st century's "electron-economy" is going to be clipped by access to REEs (especially the heavy REEs) they are now actively seeking ways around the road-block and this coupled with Australia's advanced REE mining industry and soon to be REO concentrate exporter and Rare Earth Metals producer status has changed the balance.

Clearly the race is on, we almost lost a lot of ground over the last 5 years and we can only hope that the Australian and International investing public are watching and perhaps the Australian Govt. could help with a "flow through share relief scheme" to aid Australian investors support this emerging, vital, value added, vertically integrated industry.

Rare Earth Resources by Country

The chart below published by Alkane Resources is important for two reasons.

Firstly it shows which countries out side of China have significant Rare Earth Resources Deposits and secondly the distribution of the Heay Rare Earths that are vital components for the powerful magnets required for wind turbines, hybrid and electric cars etc.

A more detailed assessment of REEs by type and country can be found here.

Rare Earth Resources by Country (Excluding China)

The USGS 2010 Resources and Reserves USA and other countries Excluding unclassified resources

The Reserves (below) as opposed to the resources (shown above) casts a different picture and reflects the current situation where many companies have not as yet converted their resources to reserve status.

(Resources : Reserves Defintion)

Rare Earth Reserves by Country Including China

(The table above is in my opinion somewhat misleading and belies the strain the world (ex-China) is about to experience when meeting its needs for Rare Earth Elements as it is based on reserves and not resources....... Thus countries such as the USA may save "face" by promoting the reserves viewpoint but also run the risk of not recognising just how relatively poor they are, in terms of resouces per capita, in these elements.)

Follow this link to the most up to date study summary of REE resources (USGS 2010) which includes some potent warnings and "between the lines" highly targeted investment advice.

Interactive Google Map of Australian Rare Earth JORC Resources

(Fly in to visit)

As Lynas Corp will become the world's swing producer of REEs (oxides and metals) in 2016, I thought it might be useful to provide some information:

Lynas Corp's Resource composition at its Mt Weld, Western Australia mine.

Note the relatively high grade of the heavy REEs.

Mt Weld: The world's richest rare earth deposit